Category: Market Intelligence

Estimated reading time: 7–8 min

The art market is often described through numbers: auction results, record-breaking sales, gallery prices, fair transactions, and indices that attempt to translate cultural value into financial performance. Yet these figures, while important, only reveal the visible surface of a much more complex system. Behind every price stands a network of reputational signals, institutional validation, collector behavior, scarcity, timing, geography, and narrative.

For collectors, investors, artists, and advisors, the central question is not simply how much a work costs today. The more meaningful question is: what forces are shaping its value, visibility, and long-term relevance?

This is where market intelligence becomes essential.

Market intelligence in the art world is not a matter of following headlines or reacting to auction records. It is a disciplined process of observing patterns, interpreting signals, and distinguishing short-term enthusiasm from sustainable market development. It combines data, context, and qualitative judgment. It requires attention not only to prices, but also to exhibitions, institutional acquisitions, gallery representation, critical reception, collector concentration, and the broader cultural environment in which an artist or movement gains recognition.

In an opaque and fragmented market, intelligence is not optional. It is the foundation for informed decision-making.

Price Is Only One Layer of the Market

A common mistake in art market analysis is to treat price as the main indicator of value. Price is visible, measurable, and easy to compare. It creates the illusion of certainty. However, price alone rarely explains the full position of an artist or artwork within the market.

Two works by the same artist may differ dramatically in value because of factors that are not immediately obvious: period, medium, scale, subject matter, condition, provenance, exhibition history, rarity, and whether the work belongs to a recognized series. A canvas from a mature and institutionally validated period will usually be read differently from an experimental work produced earlier in the artist’s career. A work included in a museum exhibition or major publication may carry a different weight from a visually similar piece with no documented history.

The same applies to artists. A rising auction price can be meaningful, but it can also be misleading. If the increase is supported by strong gallery representation, museum visibility, critical writing, and a growing collector base, it may indicate structural market development. If it is driven mainly by speculative bidding or a narrow group of buyers, the signal is weaker.

This distinction is crucial. Not every price increase represents durable value. Some markets expand because an artist’s cultural position is strengthening. Others inflate because of temporary demand, fashion, or scarcity pressure. Market intelligence exists to separate these two situations.

A sophisticated collector should therefore ask not only: What was the latest result? The more relevant questions are:

What kind of work achieved that result?

Who sold it, and where?

Was the result above or below estimate?

Was there competitive bidding?

Is the artist gaining institutional attention?

Is the market broadening, or is it dependent on a few actors?

Are comparable works available, or is supply genuinely limited?

The price is a data point. It is not the full diagnosis.

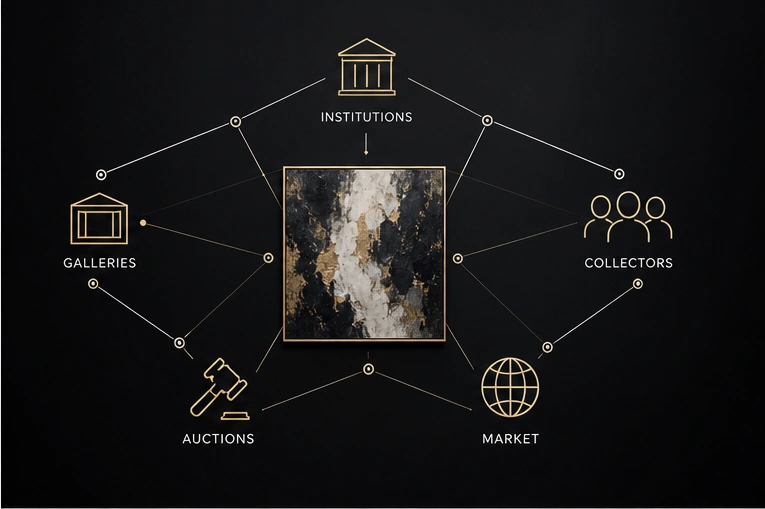

The Role of Institutional Visibility

Institutional visibility is one of the strongest long-term signals in the art market. Museums, biennials, curated exhibitions, public collections, and critical publications do not automatically guarantee financial appreciation, but they help build cultural legitimacy. Over time, cultural legitimacy can influence market confidence.

When an artist enters museum collections, participates in respected exhibitions, or becomes the subject of scholarly attention, their work is no longer evaluated purely through private demand. It becomes part of a broader art-historical conversation. This can reduce uncertainty for collectors because the artist’s relevance is being recognized beyond the commercial system.

However, institutional visibility must also be interpreted carefully. Not every exhibition has equal weight. A museum survey, a major biennial, a curated institutional group show, and a local decorative exhibition produce different levels of market significance. The quality of the institution, the curator, the publication, the critical response, and the visibility of the project all matter.

For emerging artists, early institutional attention may be a strong signal, but it should not be treated mechanically. A single museum appearance does not create a stable market. What matters is the pattern: repeated invitations, curatorial consistency, gallery support, and gradual inclusion in collections that shape discourse.

For established artists, institutional visibility can have another function. It may reactivate market interest, especially when an exhibition reframes the artist’s practice, introduces a new generation of collectors, or strengthens the historical narrative around a specific period.

In this sense, museums and institutions do not simply reflect the market. They help structure the conditions under which the market interprets value.

Gallery Representation and Market Architecture

A strong gallery does more than sell artworks. It builds an artist’s market architecture.

This includes controlling supply, placing works with serious collectors, supporting exhibitions, developing relationships with institutions, managing price progression, and protecting the artist from excessive speculation. For this reason, gallery representation remains one of the most important factors in understanding an artist’s market position.

A carefully managed primary market often develops gradually. Prices rise in measured increments. Works are placed strategically rather than simply sold to the highest immediate bidder. The gallery may prioritize collectors who are likely to hold works, lend them to exhibitions, or contribute to the artist’s long-term visibility. This kind of market discipline can be a positive signal.

By contrast, rapid price escalation without careful placement can create instability. If too many works quickly appear on the secondary market, confidence may weaken. Collectors begin to question whether buyers are committed to the artist or merely trading short-term momentum. In such cases, even impressive initial demand can become fragile.

This is particularly relevant in the market for emerging and mid-career artists. A young artist may attract attention quickly, especially if the visual language is strong and the market narrative is easy to understand. But without institutional development and responsible gallery management, early success can become a risk rather than an advantage.

For collectors, the question is not only whether an artist is represented by a gallery, but how that gallery behaves. Does it build patiently? Does it support museum relationships? Does it manage supply? Does it protect the artist’s price structure? Does it create a credible international context?

Market intelligence looks at these mechanisms, not just the name of the gallery on the artist’s biography.

Collector Behavior as a Market Signal

Collectors shape the market not only through purchases, but through patterns of commitment. The identity, behavior, and concentration of collectors around an artist can reveal much about market depth.

A healthy market usually has a diverse collector base: private collectors, institutional buyers, foundations, international galleries, and long-term supporters. When demand comes from multiple geographies and categories of buyers, the market is generally more resilient.

A fragile market, by contrast, may depend heavily on a small number of collectors or a narrow regional trend. Prices may appear strong, but liquidity can be limited. If a few key buyers stop participating, demand may weaken quickly.

Collector behavior also affects the secondary market. If collectors hold works for long periods, lend them to exhibitions, and avoid rapid resale, this can support stability. If works begin circulating too quickly after primary-market purchase, it may indicate speculative behavior. Some artists experience sharp rises followed by sudden corrections because early collectors treated the work as a trading instrument rather than a long-term cultural asset.

This is why an art advisor must read transactions contextually. The fact that a work sold is important, but the conditions of sale are equally important. Was the work sold privately or publicly? Was it consigned by a serious collector or by a short-term buyer? Was the sale part of a broader market trend or an isolated result? Did the result strengthen the artist’s market, or did it expose weakness?

In the art market, demand is not just a number. It is a structure.

Scarcity, Supply, and the Illusion of Availability

Scarcity is one of the most misunderstood forces in art valuation. A work may be rare because the artist produced very little, because important works are held in long-term collections, because a specific period is tightly controlled, or because the market has not yet released enough material to establish reliable comparables.

Scarcity can support value when it is combined with strong demand and clear art-historical relevance. But scarcity alone is not enough. An unavailable work by an artist with limited demand does not automatically become valuable. Conversely, an artist with a larger output may still have strong market value if the best works are rare, recognizable, and institutionally validated.

Supply must also be read by quality, not only quantity. The market may be saturated with minor works while major works remain scarce. Auction data can therefore distort perception if it includes too many secondary examples. A series of weak results for minor works does not necessarily mean that the artist’s primary market position is declining. Likewise, a strong result for a museum-quality piece does not automatically lift every work by the same artist.

For collectors, this is one of the most important analytical distinctions. The market does not price all works equally. It prices hierarchy: period, medium, scale, subject, quality, provenance, and relevance.

Market intelligence requires understanding where a specific work sits within that hierarchy.

Macroeconomic Conditions and the Art Market

The art market is not isolated from the broader economy. Interest rates, currency movements, geopolitical uncertainty, wealth creation, liquidity conditions, and changes in luxury consumption all influence collector behavior. However, the relationship is rarely linear.

In uncertain periods, some buyers become cautious, especially in speculative segments. Emerging artists with rapidly rising prices may become more vulnerable because collectors reassess risk. At the same time, high-quality works by historically established artists may remain resilient, particularly when they are rare and culturally significant.

This creates a more selective market. Buyers become less willing to pay for weak examples, unclear narratives, or inflated expectations. The market does not disappear, but it becomes more discriminating. In such conditions, advisory work becomes more important because the difference between strong and weak acquisitions becomes sharper.

Macroeconomic pressure can also create opportunities. Motivated sellers may release works that rarely appear. Price corrections may make certain artists more accessible. Collectors with long-term strategies may benefit from moments when short-term sentiment is cautious.

The key is not to treat the art market as immune to economic cycles. It is not. But neither should it be reduced to a conventional financial market. Art is a hybrid asset: cultural, emotional, social, symbolic, and financial. Its behavior depends on the interaction between these dimensions.

From Information to Judgment

The difficulty of the art market is not the absence of information. In many cases, there is too much information: auction results, exhibition announcements, social media visibility, gallery newsletters, art fair reports, artist biographies, collector rumors, and media coverage. The challenge is interpretation.

Not all signals have equal value. Some are structural; others are cosmetic. A serious museum acquisition has a different weight from a fashionable Instagram moment. A carefully managed gallery program differs from temporary hype. A strong auction result supported by multiple bidders differs from a single exceptional sale. A rising price can indicate either deepening confidence or unstable speculation.

Market intelligence is therefore not the passive collection of facts. It is a process of ranking evidence.

The strongest advisory decisions emerge when quantitative and qualitative signals are considered together. Data can show price movement, frequency of sales, estimate ranges, and liquidity. Qualitative research can explain why those numbers matter: who supports the artist, how the work is positioned, whether the narrative is credible, and whether the market has depth.

This is where professional advisory practice adds value. It helps clients avoid two opposite mistakes: buying only by emotion, or buying only by numbers. The first approach can ignore risk. The second can ignore art. A mature collecting strategy requires both sensitivity and discipline.

What Market Intelligence Means for Collectors

For collectors, market intelligence should not eliminate personal taste. A collection built without conviction often lacks coherence. But taste should be informed by context. The strongest collections are usually shaped by both aesthetic judgment and market awareness.

This means asking disciplined questions before acquisition:

Is this work representative of the artist’s strongest practice?

Is the price justified by comparable works?

Is the artist’s market broadening or narrowing?

Is the work supported by provenance and documentation?

Does the gallery or seller have credibility?

Is there institutional or curatorial interest?

How liquid is this segment of the market?

What are the risks if market sentiment changes?

These questions do not make collecting less passionate. They make it more responsible.

For new collectors, market intelligence helps avoid impulsive purchases based on surface appeal or persuasive sales language. For experienced collectors, it supports portfolio refinement, deaccession strategy, and long-term positioning. For artists and galleries, it clarifies how visibility, pricing, and narrative interact.

Ultimately, market intelligence is not about predicting the future with certainty. The art market is too complex for that. It is about reducing uncertainty, identifying patterns, and making decisions with a stronger understanding of the forces at work.

Conclusion: Intelligence Before Acquisition

The art market rewards patience, context, and informed judgment. It punishes superficial readings, especially when buyers confuse visibility with value or price movement with cultural significance.

A work of art is never only an object. It is part of a system: artistic practice, biography, market structure, institutional validation, collector demand, scarcity, and historical narrative. To understand its position, one must read the system around it.

That is the purpose of market intelligence.

It allows collectors and advisors to move beyond isolated transactions and toward strategic understanding. It helps distinguish durable value from temporary noise. It brings structure to a market that often appears opaque, emotional, and fragmented.

In art advisory, intelligence does not replace the eye. It sharpens it.